Common traps, missed opportunities and issues often make ESOPs seem harder and more expensive than they need to be, and undermine their impact. Fortunately, a range of simple, cost-effective solutions make ESOPs and equity-based remuneration the most attractive form of remuneration.

GRG Remuneration Insight 137

by Denis Godfrey, James Bourchier & Peter Godfrey

16 February 2022

Employee share ownership plans (ESOPs), also known as employee share schemes (ESSs), exist in almost every ASX listed company, yet we find many new clients have been paying at least 43% more than they need to for their equity-based remuneration, by failing to set up the systems and processes needed to claim a tax deduction, or maximise the value of the tax deduction. When we start to scratch the surface on how ESOP administration has been handled by new clients coming to us for help, we often find a stressed-out HR incumbent struggling to manage administration complexity, which may even be sighted as a barrier to broadening ESOP participation that can enhance the benefits for all stakeholders. In this article we highlight the key bear-traps, missed opportunities and issues that often makes ESOPs seem harder and more expensive than they need to be, and undermine their desired impact. We also share a range of simple, cost effective and easy to implement solutions to these problems that can make ESOPs and equity-based remuneration the most attractive form of remuneration. As equity remuneration rises in prominence, with a raft of companies introducing equity as part of fixed pay to address the COVID-19 crisis and skills shortages, these matters can become a key attraction and retention issues, most prominently in the technology sector.

Are you paying 43% more than you should for your equity remuneration costs (or worse?)

Many boards and HR professionals are not aware that, with the exception of the $1,000 Tax Exempt Plan, equity remuneration costs (remuneration offered under ESOPS including executive variable remuneration plans) do not count as a tax deduction for the Company. Unlike cash remuneration attributable to employment expenses, equity remuneration is amortised or expensed under AASB2 (the accounting standard) as an “opportunity cost” which does not qualify as a deductible employment cost when the Company comes to submitting its tax filings. Assuming a company tax rate of 30% and a reasonable level of profitability, cash remuneration only costs the Company 70% of recorded costs; that means that equity costs are, as a starting point, 43% more expensive to offer (30% loss of deduction ÷ 70% comparison cost = 43%).

However, when the right steps are taken, it is possible to claim a tax deduction for the market value of equity provided at the time of transfer of the benefit to the employee. If the share price has been rising, the Company can claim a tax deduction that is actually much higher than the amount expensed/amortised, meaning that a failure to take these steps could increase the unnecessary cost of equity remuneration far above the 43% level. In a fast growing company, it can in theory claim back such a high tax deduction, that the tax saved is more than the entire cost of equity recorded in the Company’s accounts i.e. effectively producing a profit. Because the effective tax deduction can produce savings exceeding 30% of the cost, this turns equity remuneration from being one of the highest cost and least attractive remuneration elements, to becoming one of the most attractive and lowest cost remuneration elements. Add to that the culture, wealth creation, tax flexibility, employee engagement and stakeholder alignment benefits of equity remuneration; the result is a recipe for the most potent remuneration tool available to any organisation which may be used as part of fixed pay, short term variable remuneration, retention and succession plans, or long term variable remuneration.

How to obtain and maximise the tax deduction

The key step in optimising the cost and tax benefits of equity remuneration is to set up an Employee Share Trust (EST). The EST must satisfy a range of requirements set out by the ATO to qualify for tax deductibility status. When equity interests are settled, the Company transfers cash equal to the market value of the equity to the EST, which typically then subscribes to a new issue of shares, repaying the money to the Company and producing a cash-flow-neutral outcome (although on-market purchase is also possible, it is a much more expensive way to go). It is this cash transfer to the EST that qualifies as a tax deduction, so the bigger the increase between the price at grant date, which is what is expensed, and the price as at the date of the cash transfer, the bigger the increase in the tax deduction that can be claimed.

This means that it is usually in the Company’s interest to allow participants to exercise their rights or options on a manual basis, as late as possible, rather than automatically at vesting. A modern Rights plan gives participants up to 15 years to exercise their interest which also defers their taxing point long term, supporting skin-in-the-game holdings (please note that some recent interpretations of ASX Guidance Note 19 have indicated that 5 years is the maximum term allowable, but if you have received such advice, we urge you to escalate the matter with your ASX compliance officer – 15 years remains acceptable and aligned with the Tax Act).

An EST may be run internally, as a subsidiary, with for example the Company Secretary or Chair of the Remuneration Committee acting as the trustee. Alternatively, share plan administration providers like BoardRoom Pty Limited (BoardRoom) offer outsourced EST solutions on a low cost, even de-coupled basis i.e. regardless of who the share registry provider may be.

The downside of internal administration and upside of expert administration

The downside of administering ESOPs and EST processes internally is the administrative complexity and lack of high volume experience in most HR teams; if participants can exercise at any time, then there need to be resources available to quickly act on requests to convert the equity interest into shares, and if there is no dedicated internal resource to manage ESOPs, mistakes are often made. This complexity often leads to minimal communications and skipping of key steps because of internal resources being stretched thin.

This goes beyond missing the tax deduction and extends to things like regular communication on numbers held, current market values, and a lack of clarity for participants regarding how to access their ESOP benefits. For this reason, many ESOP grants get put in a bottom drawer and forgotten about until someone tells the participant the interest will lapse and be lost if not dealt with in the final days before expiry. Many employees even lose their interests because of a lack of understanding of how to exercise, or when.

As well as offering EST trustee services, a 3rd party will often be able to offer outsourced administration of the whole plan from end-to-end:

- Electronic communications and plan rollout

- Online accounts with live data enabling employees to accept offers/invitations, initiate transfers, exercise rights and options, check on their holdings at any time, including key dates such as when they will vest or expire, and even sell their equity

- Electronic notices and reminders

- Automated company reporting, such as support to prepare ATO “ESS benefit” reports

- Support for ASX notice preparation

- Inputs to Board and management reporting to keep key stakeholders appraised

- Easy EST transactions that won’t be challenged in terms of tax deductibility status (you won’t, in our opinion, require a private tax ruling as this type of arrangement is so well established and widespread)

Modern technology offers a wide range of advantages at a low cost

GRG has worked with a wide range of the providers in the market over the last few years, and found that there is only one that can offer a comprehensive, flexible service on a modern technology platform backed by employee friendly mobile apps, with advanced company reporting at a consistently competitively low cost; that is BoardRoom. In fact, BoardRoom was the only provider that has been able to develop a back-end technology platform for the cutting edge unlimited employee salary sacrifice plan developed by GRG and Remuneration Technologies called the Share Save Plan, which offers employees share price fall protection at no cash cost to the Company. This is because they have invested heavily over the last 5 years in bringing employee share plan administration and EST services onto the latest technology platforms that can flexibly tailored quickly and at low cost.

Between the tax deduction, improvements in efficiency, reduction in internal workload and reduction of errors, outsourcing your ESOP EST and administration to an appropriately experienced external provider is likely to pay for itself.

A key solution for multinationals

One of the challenges many of our clients face is dealing with participants in international locations, and the uncertainties that often arise when trying to allocate shares to participants in international jurisdictions.

Using a modern integrated administration and EST platform, participants can submit an exercise notice, and have shares held for their benefit in the EST without ever taking ownership. BoardRoom offers participants the opportunity to direct the EST to sell and transfer the proceeds without ever taking direct ownership of the shares, subject to a modest broker fee. This can solve a lot of problems and perceived complexity for international ESOP roll-outs. If participants prefer to hold the shares, they can request the EST to continue to hold them, or to transfer the shares to any broker account globally.

More details on the Share Save Plan

The Share Save Plan (SSP) enables unlimited amounts of salary sacrifice (most tax efficient) to acquire plan shares with flexibility to sell shares when ever the participant wishes, up to 15 years after the Grant Date. Tax is deferred until shares are sold or withdrawn from the plan. If the Share Price falls, employees do not lose their investments, which is the main risk employees and organisations seeking to improve employee engagement face when considering ESOPs, particularly if additional company costs are to be avoided.

Call us for more information on ESTs or ESOP optimisation

GRG has deep experience over the last 20 years designing, implementing, drafting and optimising ESOPs for companies from ASX 50 to unlisted technology start-ups. If you have questions or uncertainties in the area of ESOP optimisation, call us to find out where you can get help and what the likely costs may be.

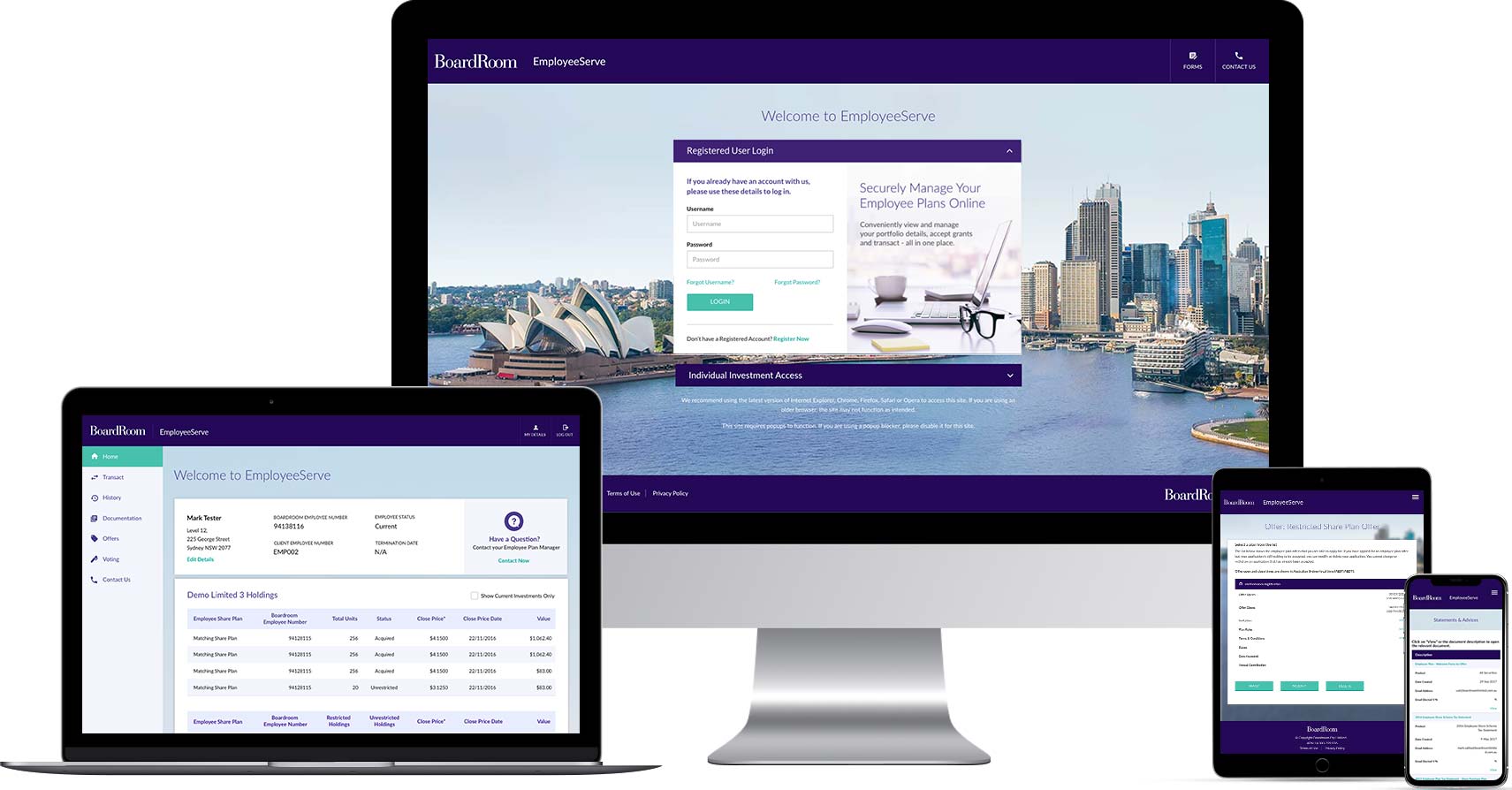

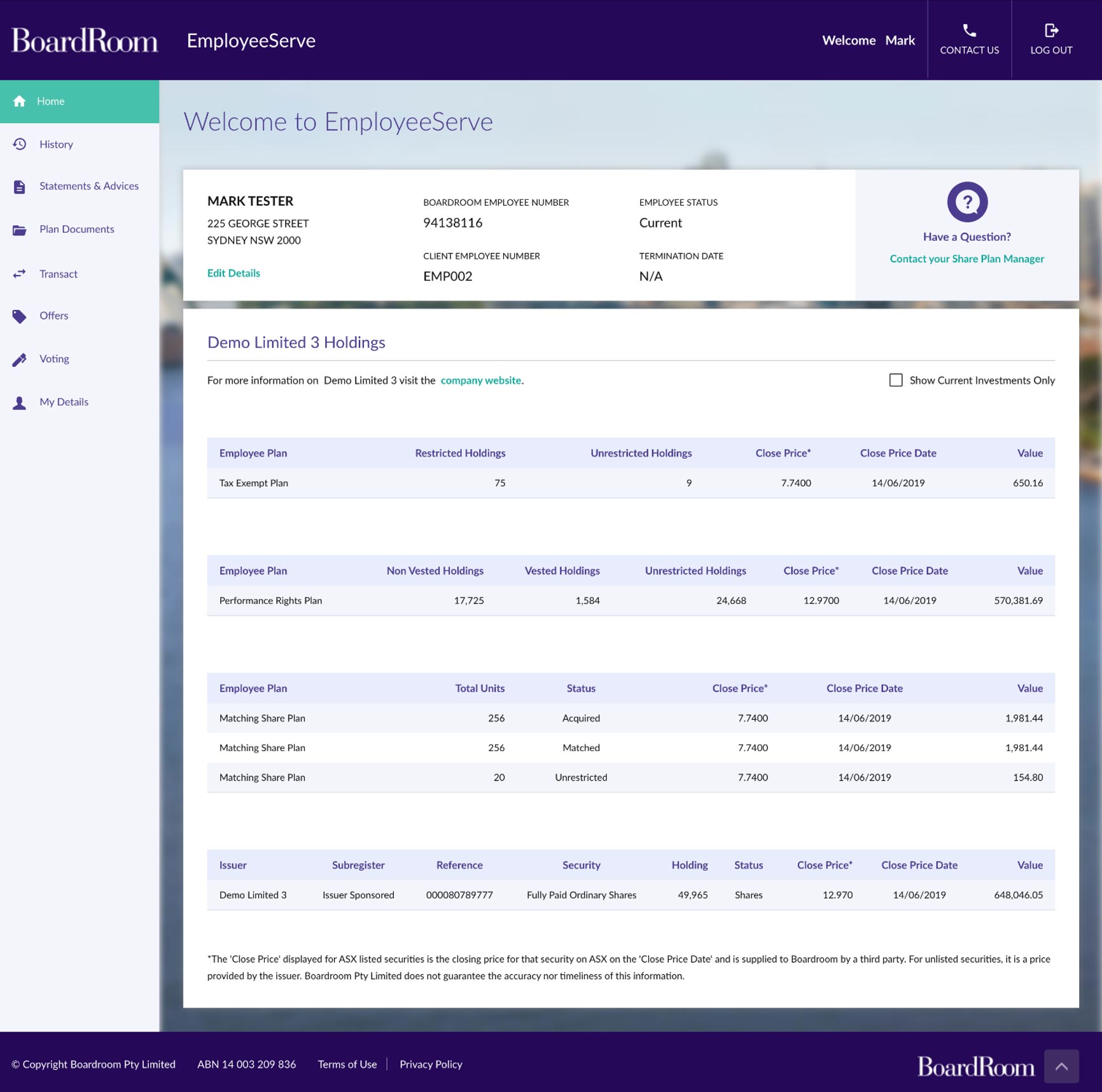

The BoardRoom dashboard

These images show what participants will see when they log into BoardRoom’s EmployeeServe, a powerful modern online digital equity platform. For more information contact BoardRoom directly.

(Click images to enlarge)

Find out more

Learn how to take full advantage of the rapid changes in employee share ownership in an information-packed webinar, co-hosted by GRG, BoardRoom and Remuneration Technologies.